People are concerned about the impact of payday advances on a credit rating. There are many reasons why you should build a credit score and protect it in the future.

If you have a poor debt repayment history, it will be challenging to obtain funding. That may entail having difficulties obtaining a home loan, getting a credit card, or financing a new car. Therefore, it is vital to be well-informed on the subject to prevent problems while borrowing money. Read ahead to learn more about how a payday loan might affect your score, thus borrowing power.

Do Payday Loans Help Your Credit?

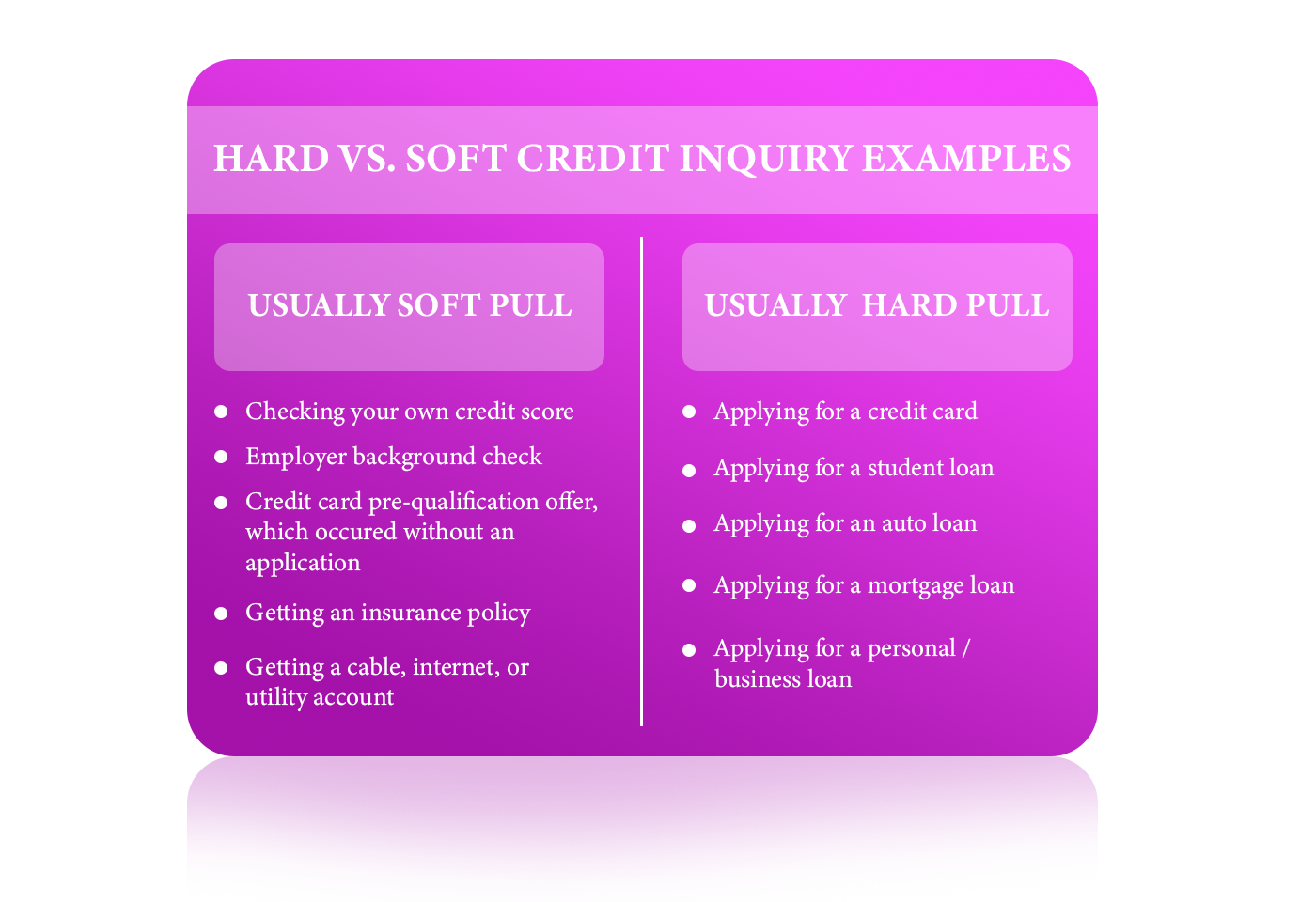

Taking out a payday loan might affect your FICO score as soon as it appears on your credit report. Applying for a cash advance loan may cause either a hard or soft credit inquiry shown on your report. Practically, hard pulls on your file are intended for lenders to see your borrowing history. For instance, if you have too many hard pulls in a short period, it may show that you regularly face financial difficulties, thus not likely to be a trustworthy borrower.

When you fill out an application, each request will be tracked independently. Thus, you should decide on the loan option you believe you may qualify for.

The most significant impact that credit pulls may have on your financial state is when you want to secure a mortgage loan. Mortgage lenders would typically interpret this to imply that you are not financially secure and won't likely qualify for large and long-term financing. You should go for loans you are most likely to be approved for. Always study the lender's requirements before submitting an application to determine your chances of approval.

Soft Inquiries

Unlike hard inquiries that are recorded on your credit report, most payday lenders offer soft checks. In plain language, this is a more limited search that shows whether you are a responsible borrower or not. Soft inquiries are occasionally offered by online lenders and lender connecting websites. Soft inquiries are often conducted for background checks and payday prequalification. However, they do not require your permission, unlike hard credit checks.

Commonly, payday advances do not appear on the financial reports of major bureaus like TransUnion, Experian, or Equifax. However, special credit reporting agencies may still have access to your cash loan history to make a proper decision. Lenders may take this into account when you seek a loan in the future. However, if you fail to pay your payday debt on time, the lender may send your debt to the collection, which will likely be reported to credit bureaus.

What if You Default on a Payday Loan?

Failure to repay a payday loan has a variety of negative consequences, including:

Extra Fees: If you fall back on your debt repayment plan or simply cannot settle the loan upon the agreed date, additional charges may incur depending on the state of lending and governing regulations. Additional charges are mainly known as nonsufficient funds (NSF) fees, and they are imposed when you do not have enough money to cover the payment.

Debt Collection: If you are 60 days past due on debt repayment, your lender will attempt to collect payment on your behalf. If you do not pay him within this period, he will almost certainly turn to a debt collection firm to recoup losses. You should anticipate the debt collection firm contacting you and sending letters frequently until the money is received. Their collection attempts will be significantly more severe than those of your lender.

FICO Score Drop: Paying off payday debt on time won't negatively affect or build your credit. However, as we have mentioned before, once you get your debt sent to collection, your FICO score will suffer.

Legal Consequences: Even if you just owe a modest amount of money, the debt collector may sue you. This might result in foreclosures and perhaps wage garnishment, depending on the state of your residence.

Is It Worth Taking Out a Payday Loan?

Credit card companies and banks are obligated to record on-time payments when a borrower obtains a loan. On the other hand, payday loan companies are not compelled to record the financial conduct of their customers.

However, there are financial factors to be mindful of when it comes to payday loans. Although getting a payday advance does not necessarily harm your credit score, special circumstances may make it happen. As a result, every loan you take out must be well-weighted based on your capacity to repay the debt.

The Key Features and Risks of a Payday Loan

Many people are drawn to online loans because it’s the most hassle-free way to borrow some money nowadays. This is due to the fact that the application process is typically quite rapid and may be completed within a few minutes. Plus, payday lenders do not frequently perform credit checks. Also, unlike most banks, payday lenders accept bad credit holders.

However, payday loans are notorious for high-interest rates and harsh late-payment penalties. Borrowers who do not make timely payments may watch their debt grow and grow until it is out of their control.