.jpg)

Suppose you need to borrow money at some point in your life to fund a large home improvement project, pay your taxes, or cover an unforeseen medical emergency. You might even want to consolidate debt by taking out a loan with a better interest rate. A personal loan or a line of credit, depending on your situation, may assist you in achieving your objectives. However, while both methods might provide you with the funds you need, they operate in quite different ways.

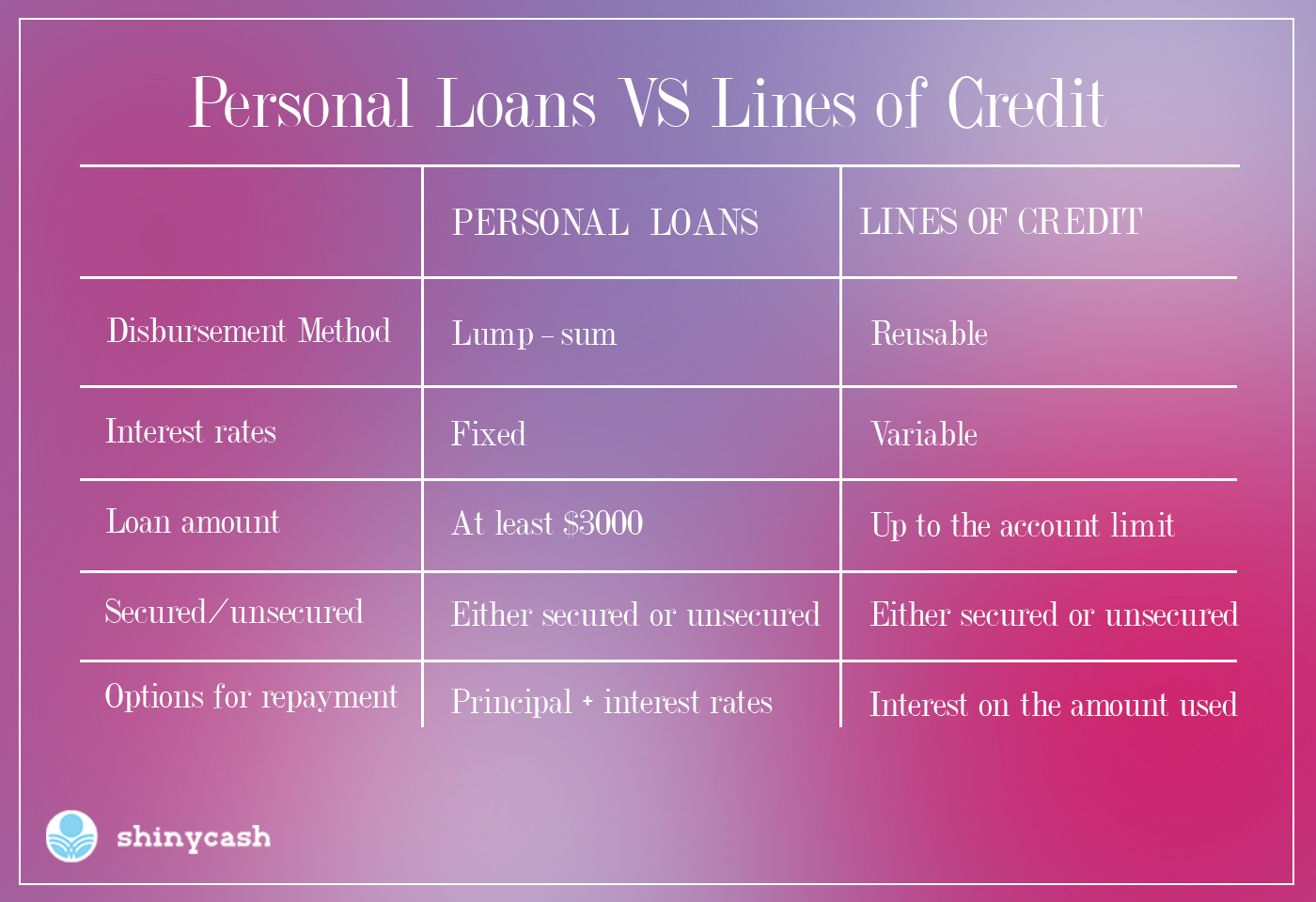

About Personal Loans

A personal loan enables you to borrow money to cover personal expenses and repay it over time.

Personal loans are available as secured or unsecured loans. As a condition of borrowing, a secured personal loan requires some form of collateral. To borrow money with an unsecured personal loan, no collateral is required. Banks, credit unions, and online lenders can provide qualifying applicants with both secured and unsecured personal loans.

Personal loan interest rates are usually fixed, ranging from 3 to 36 percent. Rates are determined by your creditworthiness, which means that if you have good credit and a steady job, you can get a better deal.

About Lines of Credit (LOC)

A line of credit (LOC) is a set amount of money that can be borrowed at any time. In the case of an open line of credit, the borrower can take money out until the maximum is reached, and as money is repaid, it can be borrowed again. Thus, when a borrower is authorized for a line of credit, the bank or financial institution gives them a specific credit limit, which they can spend in full or partly over and over again. This creates a revolving credit limit, which is a far more versatile borrowing tool.

An interest rate on a line of credit is variable and fluctuates depending on the prime rate. If the prime rate rises, the interest rate on the line of credit will increase as well. Borrowers can expect interest rates of at least 10%.

The fundamental advantage of a line of credit is its built-in flexibility. Borrowers can request a specific amount, but they are not required to utilize it all. Instead, individuals can customize their LOC expenditure to their particular needs, paying interest only on the amount they draw, not on the whole credit line. Borrowers can also change their payments amounts based on their budget or cash flow as needed.

How Much?

Your income and credit score determine the amount you can borrow and the maximum amount a lender can lend. You receive your entire loan amount in one single sum when you take out a personal loan. You can borrow up to your account limit on a line of credit. If your account is in good standing, however, you can make payments to reduce the balance and then borrow up to your account limit once more.

Application

A personal loan or a line of credit application follows a similar procedure. To evaluate whether granting credit to you is a reasonable risk, a lender will first look at your credit report and score, as well as your income and assets. Your chances of getting approved for either sort of financing are better if you have good credit. The most significant distinction between a personal loan and lines of credit is that with a personal loan, you must know how much money you wish to borrow upfront.

In a Nutshell!

Considering the distinctions between personal loans and lines of credit can go a long way toward assisting you in selecting the best option. A personal loan varies from a line of credit. You borrow a defined amount of money and return it over a certain period with a predetermined payment amount. When opposed to lines of credit, personal loans are easier to budget for. On the other hand, lines of credit can give you more options when it comes to borrowing. For example, you can borrow up to your credit limit on a line of credit, refund the amount, and borrow again.