Although it's quite tricky to get a car loan with less-than-perfect credit, it's still possible. While having solid credit may enable you to qualify for a loan with reasonable financing terms, there are still solutions accessible for those with derogatory marks on a financial report. Because no minimum score is needed for a car loan, borrowers only need to locate a suitable lender to get quick financing. As per Experian research, Americans with bad (scores below 670) or no credit ratings usually opt for the same number of vehicle loans as those with higher-good or excellent scores.

Steps to Take Before Opting for a Car Loan with Bad Credit

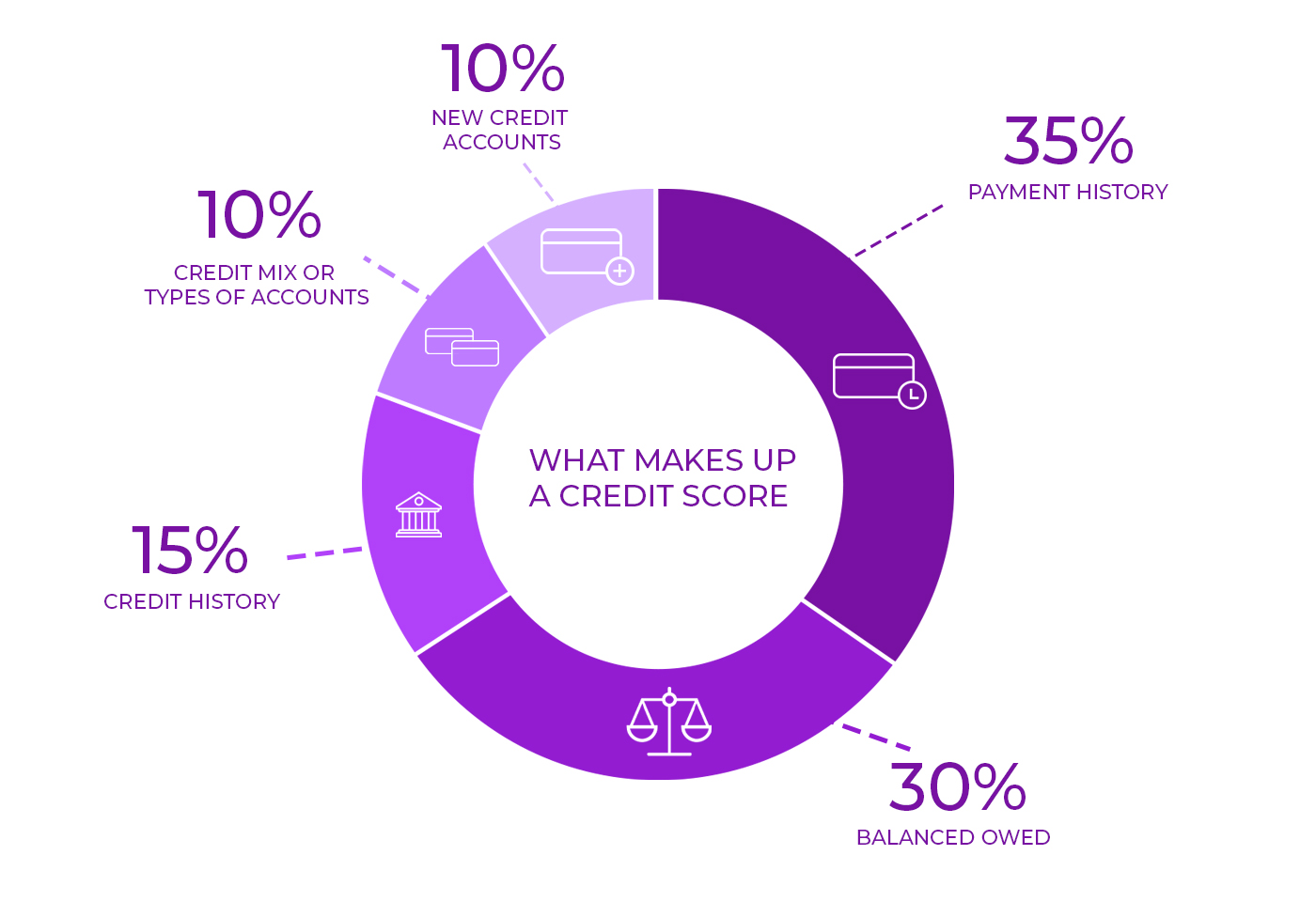

Indeed, a credit score is one of the most focal variables lenders consider when defining whether or not to qualify for a car loan. According to a FICO Score range (300-850), a score is deemed bad or fair if it falls below 670. With a bad credit score, you won't likely qualify for most financing tools; however, with careful planning and study, you may find financing that works best for you. Here are some things to do to increase your chances of loan approval, thus lowering your borrowing costs.

Examine Your Score and Improve it if possible!

It's always worth examining your financial state before opting for quick funding or making a large purchase. At Annualcreditreport.com, you can get a free copy of your report to help you understand where you are. Checking your score ahead of time helps make changes and perhaps raise your score before submitting a credit request. In addition, improving your score enables you to obtain better alternatives with cheaper interest rates, which save you money in the long run. Here are some suggestions for increasing your rating, thus credibility:

Make on-time payments on all debts: The payment history is a focal factor (accounts for 35%) that goes in FICO score calculation, and having a clean record is the simplest method to boost your credit. If you have delinquencies or debt in collection, try to pay them off as well.

Reduce the amount you owe: Reducing debt amount may help improve your financial state and lower the credit utilization ratio. To calculate amounts owed, divide your overall debt balance by your credit limits. You need to keep the utilization ratio below 30%, ideally 10%, for the best result.

Take advantage of self-reporting: The length of your credit is also a considering factor for most lenders to understand how successfully you managed your debt previously. Thus, having a short repayment history may be at a disadvantage. However, you can help boost your rating by adding information or fixing errors on your report. Experian Boost and UltraFICO may be an excellent fit to supplement a weak profile with additional financial information. Plus, both are free of charge.

Put Down Payment

When you purchase a car, you will normally make a down payment (usually 20% for new and 10% for used cars). This deposit is deducted straight from the offered amount, while the remaining sum should be repaid over time in equated money installments (EMI). When purchasing a car, the more is your down payment, the less expensive is your financing. Furthermore, a bigger down payment minimizes risk to your lender, helping you achieve better terms, thus saving on interest and fees.

Determine How Much You Can Afford

When opting for a loan, you must consider key inputs: down payment and the cost of car ownership. On average, the cost of owning a vehicle may include your debt payment, insurance, petrol, and maintenance. Therefore, considering the total car expenses is the primary step to determine how much you can afford monthly. The costlier your vehicle is, the bigger your monthly and down payments are.

Get Preapproval for a Loan

Before submitting your credit request, you can get a pre-approval to know how much a lender may be willing to offer the best on your financial state. Pre-approval may give you a clear picture of what you can afford and ease the stress of whether or not you can qualify for a certain car loan. This alone may help to negotiate better credit terms and interest rates.

Look Around for the Best Deal

When you are ready to fill out a loan request, you should first perform some research. If you're experiencing trouble, receiving funding from a traditional lender may be nearly impossible. Thus, try to locate lenders that specialize in bad credit financing. However, consider that these lenders may charge higher interest rates, but they assist customers with bad ratings to qualify for car loans.

While you look for the best financing terms and lower interest rates, you may easily wind up dealing with multiple lenders. Be informed that making too many requests may cause a credit score drop because of hard pulls. Thus make sure you apply to various lenders for a couple of weeks (multiple inquiries will be merged into one) or simply go for loan prequalification.

Where Can You Get a Car Loan with Bad Credit?

Before submitting a car loan request, you need to consider all available options. Here are the most prevalent forms of vehicle financing:

Captive financing: This form of funding is handled directly by the manufacturer, meaning that you not only buy a car directly from a dealership but also finance the loan. Captive financing is also available when buying a used car. This is suitable for those with fair ratings.

Dealer financing: Usually, car dealers support a wide range of lenders to discover and get financing for your vehicle. After you qualify, you may be presented with multiple loan alternatives from which you may select the best fit. This option is quite advantageous since it boosts your chances of credit approval by sharing your information with multiple lenders.

Bank or credit union: Getting a car loan from a bank or credit union is also a viable option since you are likely to qualify for the lowest interest rates. They are usually paid through monthly installments straight to your bank. This may be a useful alternative for those who already have dealt with traditional lenders since they may ignore faults and rely on your experience with the organization.

Online lenders: Auto financing is now available from online banks and financial organizations. The application process for these loans is often completed entirely online. To locate one of these deals, conduct a general web search, focusing on organizations that operate entirely online. You may also turn to an aggregation website, which allows you to submit a single request and obtain many financing offers.

.jpg)

.jpg)